Free Quote Call Today

(877) 852-4327

Hospitality & Liquor Liability Insurance

Comprehensive Package Policy | Stand Alone Liquor Liability Policy

To Get a Quote

Simply Complete the Quick Form below

Why Do You Need Liquor Liability Insurance?

- You may be liable for the actions of intoxicated or underage persons you serve

- The negligent service to an intoxicated or underage person can produce substantial verdicts or settlements

- Employers may be held liable for the actions of employees who sell or serve alcohol in violation of state laws

- Even if you are not found liable, it will cost thousands of dollars to defend against a claim

- The average legal cost to defend a claim is $150,000

- Underage drinkers make up a significant portion of alcohol-related traffic accidents

- Even if you sale alcohol for off-premises consumption (Retail Store), you could still be held liable for an illegal or improper sale of alcohol! (Example: Sale to minor or someone visibly intoxicated)

- A Liquor Liability Insurance is a known annual expense compared to the unknown financial impact of defense costs and court verdicts

What Type of Businesses or Entities Need Liquor Liability Insurance

- Restaurants (Fine Dining, Family Restaurants, BYOB, Fast Food)

- Retail Store: Liquor Stores, Convenience Stores, Grocery Stores, Deli Shops

- Nonprofits: Social Clubs, Private Clubs, Fraternities

- Bars / Taverns, Night Clubs, Adult Entertainment Clubs, Lounges

- Caterers, Concessionaires, Banquet Halls, Bartending Services

- Special Events: Host Liquor Liability

Retail Liquor Store Liability (Package)

- On one policy we can offer:

- Property including inventory

- Equipment Breakdown

- General Liability

- Crime

- Liquor Liability

- Loss of Income

- Non-owned & Hired Auto (no delivery)

- No Liability Deductible

- Coverage for New Ventures

- On premises Tasting / Sampling

- Delivery, Internet Sales, Drive-Thru is permited

- Prior Loss or Violation History is acceptable

- Credits & Discounts for Alcohol Awareness Training

- Credits & Discounts for Electronic ID Scanners

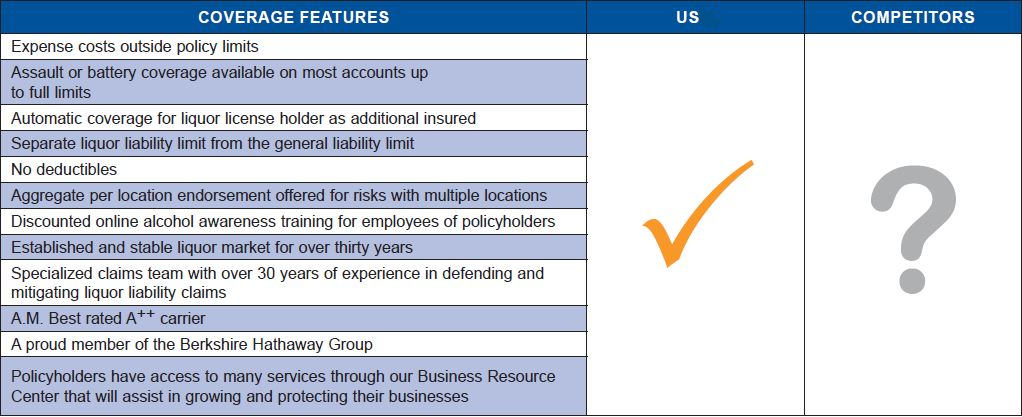

Not All Liquor Liability Insurance Policies are Equal:

Make sure your policy has these features:

Liquor Liability Product Assault or Battery

"Assault" means the threat or use of force on another that causes that person to have apprehension of imminent harmful or offensive conduct, whether or not the threat or use of force is alleged to be negligent, intentional or criminal in nature.

"Battery" means negligent or intentional wrongful physical contact with another without consent that results in physical or emotional injury.

Consider the following Actual Claim Examples: (It could happen to you)

- A minor using a fake I.D. was drinking at a restaurant. While on the dance floor, an argument broke out with another patron. The minor hit the other patron near the eye with a beer bottle causing significant injuries and requiring eye surgery. The total claim resulted in $185,000 in damages split between the general liability and liquor liability carriers, and defense costs totalled $98,000.

- While watching a football game at a local bar, three friends became involved in an altercation with another patron who

was intoxicated. During the fight, the other patron stabbed one of the friends, and the friend was later pronounced dead at the

hospital. The policy limit of $300,000 was exhausted and defense costs totalled $25,000. - A woman and a group of friends attended a hockey game where they each drank two beers. They later consumed more

beer at a neighborhood bar. While in line for the restroom, the woman got into a fight with another patron. The woman

was escorted from the bar by the bouncer, and after showing resistance, she was picked up by the bouncer and thrown

to the ground. She sustained multiple injuries and required surgery. The woman filed suit against the bar, claiming her

injuries stemmed from the over service of alcohol. The claim settled for $90,000 and additional expenses totaled $15,500. - Two patrons “bumped” into each other at the service bar of a hotel. Both showed signs of intoxication and one “sucker punched” the other. The injured patron sustained a severe head trauma, resulting in permanent injuries. The policy limit of $100,000 was exhausted and defense costs exceeded $37,000.

- An intoxicated patron hit another man in a bar. The victim did not retaliate and left the bar to go home. The intoxicated patron and his friends followed the man and ended up assaulting him. The man was in a coma for four months and was subsequently institutionalized due to the severity of his injuries. The claim was settled for $405,000, the remaining policy aggregate limits. Defense costs exceeded $17,000.

Retail Store Liquor Liability

(Actual Claim Examples)

- A 16-year-old male purchased beer from a local retail store

and no one checked his ID. He took the beer to an underage

drinking party. Several hours later, his 20-year-old sister arrived to take him home, and she also consumed some beer.

After they left, she lost control of her convertible, which flipped

over and killed her brother.

The mother of the deceased filed suit against the retail store. Even though the person who caused the accident did not actually purchase the alcohol, the retail store was held liable due to the illegal sale to a minor. The claim settled for $580,000 in damages, and expense costs totaled an additional $100,000. - A 19-year-old was consuming beer he purchased at a local gas station when he crashed his car into a tree. The passenger in his vehicle sustained significant brain damage, fractured legs and other internal injuries.

The passenger sued the gas station for selling alcohol

to a minor. The claim settled for the full policy limits of $1,000,000. - A convenience store denied service to a patron who appeared

intoxicated. The patron was later involved in an automobile accident. Despite denying service, the convenience store was named in the suit.

Ultimately, the convenience store was not found liable, but expense costs totaled $75,000. - An adult woman purchased a bottle of alcohol at a local liquor store. Her husband previously instructed all nearby stores not to sell alcohol to her because she was an alcoholic. The day after purchasing the bottle of alcohol, the woman drowned after falling or jumping off a bridge.

The deceased’s family brought suit against the liquor

store for selling alcohol to a known habitual drunkard, and the case settled for $850,000.

Liquor Liability for Non-Profits & Social Clubs

- Limits up to $1,000,000/$2,000,000 available

- Monoline Liquor Liability Product

- automatic coverage for the Liquor License holder as an additional insured

- No deductible

- Employees and club members covered as Insureds at no

additional charge - Landlords may be added as an additional insured for a nominal

additional premium - Terrorism coverage included for no additional premium

- Preferred Pricing for Clubs with certain qualifications

- Credits available for responsible clubs with a formal

third-party server awareness training program - A.M. Best rated A++ carrier

We are an Authorized Retailer for

Social Media

Contact

Ph: (714) 453-0700

421 S. Main St

Orange, CA 92868